The Big Bath of Tim Wentworth 🛁, or the Worst Day in Walgreens' History

Also, RIP VillageMD. 🪦

Welcome to AI Health Uncut, a brutally honest newsletter on AI, innovation, and the state of the healthcare market. If you’d like to sign up to receive issues over email, you can do so here.

Yesterday marked the worst day in Walgreens’ stock history. This company has endured the early 1980s recessions and hyperinflation, the 1987 “Black Tuesday” (the worst day in the stock market’s 250-year history), the international currency crisis of 1997-1998, the dot-com bubble burst of 1999-2000, and the Great Financial Crisis (GFC) of 2007-2008.

None of these events even remotely compare to the bloodbath that occurred yesterday. WBA stock nosedived by 22.2%, crashing to a level not seen since June 11, 1997.

Coincidentally, this was also the day Tim Wentworth, the new CEO of Walgreens, became the happiest man on Wall Street. He wants WBA to sink as much as possible. But even he didn’t expect the biggest drop in WBA history. He must still be jumping up and down on his super mega yacht as we speak.

Your eyebrows may be way above your forehead right now. Let me explain. It’s actually a fascinating story.

When Walgreens’ board fired its then-CEO Roz Brewer for making one of the worst acquisitions in stock market history, VillageMD, and bringing the company its first-ever loss in its 122-year history (ironically, Tim’s first nine months are even worse) in October 2023, they hired Tim Wentworth as the new CEO. What was Tim’s first order of business? To sink WBA stock price, of course.

Hear me out.

It’s the oldest magic trick in the book, dissected in countless Harvard Case Studies. But kudos to Tim Wentworth for mastering it without setting foot in a business school. (Personally, I share Tim’s skepticism towards douchy degrees like MBAs and CFAs. I’m with him on that one – wink 😉.)

Here’s how the trick works. 🎩 Blame all past failures on your predecessor. Write off all the assets acquired before your time (think VillageMD and Summit/CityMD). Announce massive cost cuts, like Tim’s bold $1 billion slash in Walgreens’ healthcare business. Watch the stock price plummet. Don’t forget to pamper the cat while whispering “Excellent”. 🐈

In the snooty MBA textbooks, this trick has many names: “Big Bath,” “Taking a Bath,” “Kitchen Sinking,” “Cookie Jar Accounting,” “Clearing the Decks,” and the dramatic “Coup de Jarnac.”

Why does the new CEO pull this seemingly self-destructive move on their own stock? It’s simple. Follow the money.

“Big Bath” 🛁 is a semi-legal strategy where a new CEO announces bad news or takes actions that cause the company’s stock price to drop significantly. This sets a much lower baseline stock price, allowing the new CEO to receive stock options and other equity-based compensation at a lower exercise price. If the company’s performance improves, the stock price increases, and the CEO stands to gain significantly from the appreciation in stock value.

Should be illegal, but hey, we live in a country where members of Congress are the best portfolio managers and SEC lawyers become general counsels of the same investment firms they used to police. So what do you expect?

Here’s what Tim Wentworth has “accomplished” so far:

🛑 In an interview, he mentioned putting VillageMD “on a diet.” He’s announced the closure of 60 clinics so far. In reality, as I explain below, there will be a winding down of VillageMD clinics over the next few years.

🛑 He suggests that VillageMD is not expected to make a profit in the near future. Translation: “The previous CEO bought this piece of sh*t, and I’m not about to give rosy expectations.”

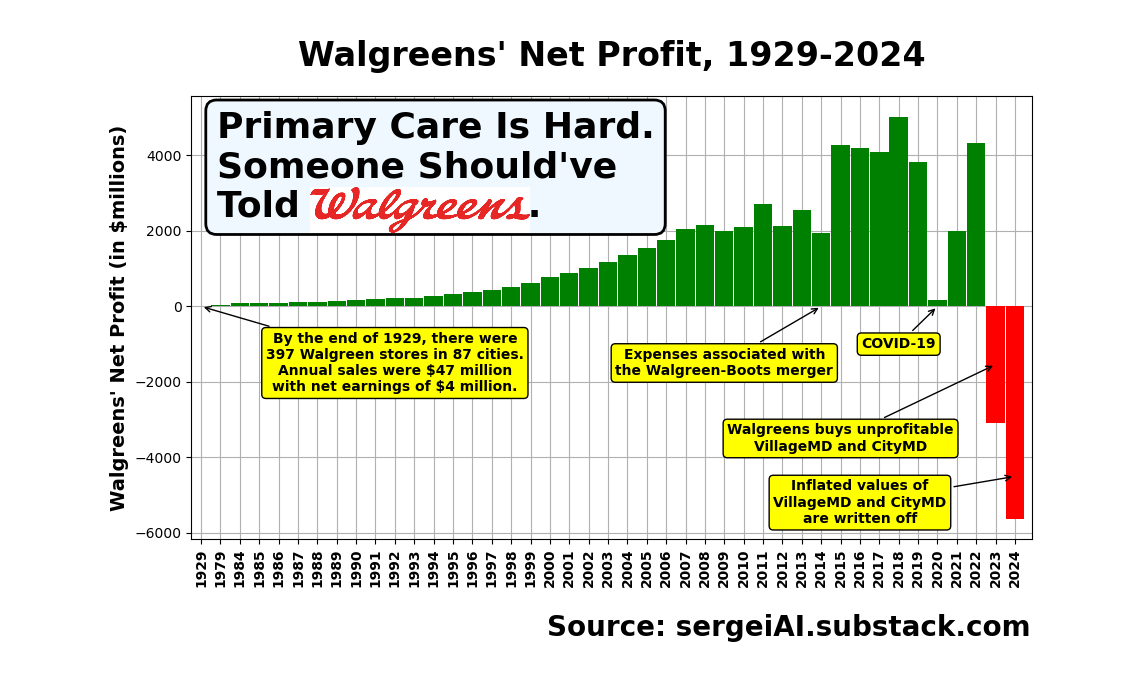

🛑 To support his statement, he wrote off $5.8 billion in VillageMD goodwill impairment, corresponding to a $12.4 billion impairment for the total value of VillageMD. This makes 2024 the worst fiscal year in Walgreens’ 123-year history, even worse than the previous year. Walgreens paid a total of $9.7 billion for both VillageMD and CityMD, and it’s now worth only $5.5 billion according to Walgreens’ regulatory filings. Walgreens has lost 43% on its VillageMD/CityMD investment in just 2 years! The members of Congress must be laughing all the way to the bank. Even this number doesn’t make any sense as I explain below.

🛑 He announced the closure of at least 1300 Walgreens drug stores in the U.S. and UK.

🛑 He introduced a $1 billion cost-cutting program to “boost profitability in the healthcare business.”

🛑 He dramatically cut the company’s profit outlook.

🛑 Statements like “We are at a point where the current pharmacy model is not sustainable” would definitely affect the stock price in one direction - down.

🛑 Tim can’t openly blame the previous CEO, so he blames Walgreens customers, saying things like “Our customers have become increasingly selective and price sensitive in their purchases.” Assigning blame is obviously nonsense, but again, it doesn’t matter. Tim’s goal is to sink the WBA stock price. In reality, this bad situation for Walgreens started 10 years ago with the acquisition of Alliance Boots and the assumption that European spending habits are as crazy as those among American consumers. It turned out they are very far apart. The situation was further aggravated by the almost $10 billion spent on the acquisition of VillageMD and CityMD. The irony is that $10 billion is currently the total market value of the whole company!

Short of setting Walgreens stores on fire, Tim Wentworth has done everything in his power to drive the WBA stock price down to its lowest level since June 11, 1997, so his stock options are struck at the lowest price humanly possible.

RIP VillageMD 🪦

By impairing VillageMD’s total value by $12.4 billion (i.e., writing down $5.8 billion of its value on the books), Walgreens is implying the book value of VillageMD on its balance sheet is $5.5 billion. This is absurd, given the entire company’s market value is only $10.52 billion, as of yesterday’s close.

Teeny-Tiny VillageMD certainly doesn’t represent 52% of Walgreens’s business. So brace yourselves for more impairments and billions in losses in 2024 and 2025.

The fair value of VillageMD on Walgreens’ balance sheet is, at most, $600 million, considering the entire company’s market cap is $10.52 billion.

It’s amusing to revisit statements made by Walgreens only 17 months ago:

“Walgreens also raised its fiscal year 2025 sales goal for its U.S. healthcare business to between $14.5 billion and $16 billion from $11 billion to $12 billion previously. That business segment is now expected to achieve positive adjusted EBITDA by the end of fiscal year 2023.”

Well, that clearly didn’t pan out. Walgreens’ healthcare business isn’t going to be profitable by the end of fiscal year 2023, or 2024, or 2025, and its sales are a mere $8 billion, not $14 billion.

From Walgreens’ earnings call on June 27, 2024:

Question:

“Given the plan to exit VillageMD and the idea that value-based strategies often take a few years in order to get profitable versus some of your nearer-term profitability goals, what’s the forward take on the need to be in the value-based strategy for the best of U.S. healthcare?”

Answer:

“With respect to value-based care, we have already articulated that we don’t have plans to continue to invest in brick-and-mortar-owned primary care practices.” —Mary Langowski, President of Walgreens, U.S. Healthcare.

They also implied they do not expect VillageMD to be profitable anytime soon.

It just doesn’t look good for poor ol’ VillageMD, and increasingly, for Walgreens.

Was the Walgreens News Really That Bad for CVS?

It is obvious from this chart that the market believed Tim when he said there are “significant challenges in the U.S. retail pharmacy business, stemming from a worse-than-expected consumer environment and challenging pharmacy industry trends.”

So the market sold out CVS as well, following the centuries-old stock traders’ rule, “Sell first, ask questions later.”

I disagree. The Walgreens’ news is not as bad for CVS because, unlike Walgreens, CVS has the SopranoRx business: the Caremark PBM mafia family and the Aetna insurance mafia family.

Plus, we have to adjust for Tim’s overzealousness to throw away everything but the kitchen sink.

Conclusion

Walgreens is a Harvard Business School case study begging to be written. It’s a cocktail of corporate intrigue, negligent due diligence, and financial missteps. Picture this: an American entrepreneur builds a company on principles of frugality, efficiency, and cost-cutting. For 122 years, the company never experienced a loss, weathering depressions, wars, and recessions. Enter the new management, deciding it’s a brilliant idea to buy a European company and Americanize it. That’s where the chaos begins.

One CEO thinks it’s brilliant to ditch a core business that’s rock-solid for over a century and dive into something they know jack about, blowing a fortune they didn’t actually have. Meanwhile, another CEO is busy tanking his own company’s stock price to line his pockets, subtly suggesting his predecessor overpaid massively for a failing asset. If this isn’t the most riveting Wall Street thriller, I don’t know what is.

Healthcare corporations are constantly pressured by their boards to “conquer primary care.” Yet, these corporate geniuses fail to grasp that primary care is not like Scrub Daddy or Bombas Socks: it’s not scalable. You can’t just mass-produce and flip primary care to the next bidder. It’s not a commodity to be financialized by these CEOs who think they can fit primary care into a spreadsheet. There are social and emotional determinants at play, not just the allure of dollar signs.

Primary care is hard. It’s deeply human. This isn’t something you can grasp by sitting in a boardroom, staring at PowerPoint slides.

Charles R. Walgreen must be doing somersaults in his grave…

👉👉👉👉👉 Hi! My name is Sergei Polevikov. In my newsletter ‘AI Health Uncut’, I combine my knowledge of AI models with my unique skills in analyzing the financial health of digital health companies. Why “Uncut”? Because I never sugarcoat or filter the hard truth. I don’t play games, I don’t work for anyone, and therefore, with your support, I produce the most original, the most unbiased, the most unapologetic research in AI, innovation, and healthcare. Thank you for your support of my work. You’re part of a vibrant community of healthcare AI enthusiasts! Your engagement matters. 🙏🙏🙏🙏🙏

I worked indirectly a few years ago with the VillageMD folks in TX in the ACO formation area, and even before the Walgreens buy they were marked by a certain arrogance. But they were also good at Medicare value based care and turned in great results in spend and quality.

Their leadership certainly made out on Roz's dime! And then getting them to finance the Summit Health buy was the whip cream and sprinkles from what I heard! But there goes VillageMD and all the doctors, staff, and patients thet built up for years...what about them now on the block? Who will buy them?

One thing that didnt get a ton of attention was Boots' managing director in July announcing his Nov departure, as WBA announced it *wasn't* selling Boots. Meanwhile CVS is flogging Oak Street all over TV and social. It gets curiouser.