Cigna Pays Its CEO $663,318,942 Amid Underperforming Stock: Shareholders Deserve an Explanation

With interest and clever tax tricks, David Cordani's net worth might well exceed $1 billion.

With interest and clever tax tricks, David Cordani's net worth might well exceed $1 billion. This could make him the first business executive in history to amass such wealth without founding a startup, starting a business, or inventing a product. Instead, his fortune would stem solely from executive compensation, effectively capitalizing on the increasingly unbearable insurance premiums paid by American families each month. Cigna has been paying Mr. Cordani record-high compensation, while the company's stock has underperformed. Notably, since Cordani became CEO, Cigna's stock has performed worse than its peers for 10 out of the 14 total years, including 5 of the last 6 years.

I'm not against humans earning what they deserve, but in this case, I'm not so sure for the following reasons:

1️⃣ Cordani is the only CEO I'm aware of who became a billionaire without being a founder, an inventor, or involved in a family business. All he did to become a billionaire was collect his Cigna paycheck during a time when Cigna’s customers have suffered. National American family health insurance premiums increased from $13,375 in 2009, when Cordani became CEO, to $23,968 in 2024. This is a 5% increase per year, far exceeding the inflation rate and becoming an unbearable burden for many Americans (Source: KKF). And you're still not done. You have to meet your deductible, pay co-insurance, co-pay, potential out-of-pocket expenses, and other unpredictable costs. Due to these skyrocketing health insurance costs, tens of millions of working Americans are uninsured or underinsured. About 1 in 5 Americans has medical debt in collections, and medical costs are a common cause of bankruptcy (Source: Marshall Allen on Substack.) Most Americans cite medical expenses as the leading cause of personal bankruptcy filings, and among those, 75% actually have health insurance. Cigna and its CEO have contributed significantly to this crisis, in my opinion.

2️⃣ While Cordani amassed all this wealth and became the richest non-founder executive, Cigna stock underperformed compared to its competitors (as defined by Cigna in its most recent proxy filing to the SEC). Some shareholders may be blindsided by the fact that Cigna stock went up during Cordani's tenure as CEO. However, the primary reason for Cigna’s stock rise is the overall upward trend of the stock market, which has reached historic highs. What Cigna shareholders should be concerned about is Cigna's performance relative to its closest competitors, where it has underperformed. In other words, under Cordani’s leadership, Cigna’s shareholders would’ve been better off investing in Cigna’s competitors, and at a lower risk.

3️⃣ I believe David Cordani may have “misrepresented” his resume to artificially boost his performance, potentially affecting his compensation. I will explain this below.

Let’s delve deep into the fascinating story of David Cordani and Cigna’s mismanagement. Here’s the outline of this article:

1. Cigna Stock Underperformance

2. Cigna Headwinds

3. Cigna's Tactics to Artificially ‘Pump Up’ The Stock Price

4. Cigna’s Closest Competitors

5. Cigna’s Executive Compensation

6. How Did David Cordani Become a Billionaire?

7. David Cordani’s Tax Tricks

8. David Cordani’s Termination Clause

9. Cigna’s History of Violations

9.1. Cigna sells patients’ lab results and claims information to WebMD.

9.2. Cigna’s AI stress tool: shitty and potentially hazardous.

9.3. Cigna’s AI algorithm automatically denies claims. Cigna “doctors” concur without even looking.

10. Wall Street Analysts Are in Bed with Cigna’s Management

11. How Did David Cordani “Misrepresent” His Resume?

12. My Take

1. Cigna Stock Underperformance

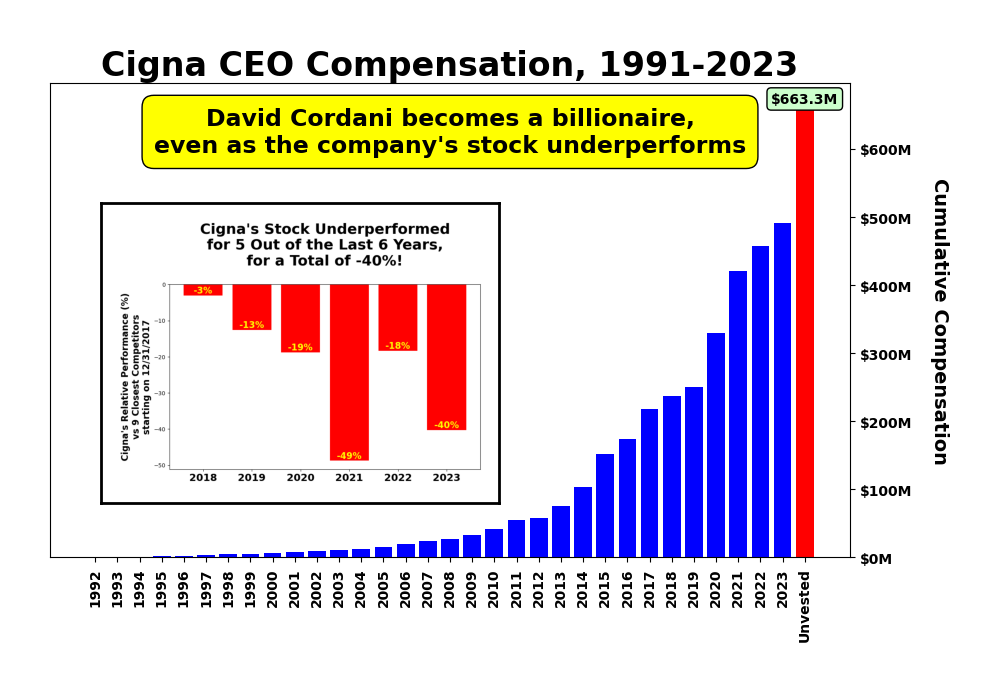

This Tuesday, January 9, 2024, at the #JPM2024 healthcare conference in San Francisco, Cigna CEO David Cordani assured the crowd during a seemingly pre-rehearsed interview moderated by J.P. Morgan healthcare analyst Lisa Gill, that 2023 was another great year for Cigna, a claim that was false. It's remarkable how questions can be selected to create an overly positive impression.

The reality is that 2023 was one of the worst years under Cordani's leadership. The stock returned -8.0% for the year, while Cigna’s nine closest competitors (as identified by Cigna itself) returned an average of 2.0%. Meanwhile, the broader healthcare sector, represented by the SPDR ETF (ticker XLV), returned 2.1%, and the broader market, as represented by the S&P 500, returned 26.3%.

Among its nine closest competitors, Cigna has underperformed in 10 out of the past 14 years since Cordani assumed the CEO role, including in 5 of the last 6 years.

Cigna has been lagging behind its competitors for years, a dismal performance streak that’s become almost embarrassingly routine. For example, since the Strategic Performance Share (SPS) executive stock award program kicked off in 2018, Cigna has consistently underperformed its peers on a 3-year rolling basis. Every. Single. Year. It’s not just underperformance. It’s a masterclass in mediocrity that’s surely infuriating to them.

The Cigna board, witnessing this relentless underachievement, has been scratching their heads over what the company should focus on. They’ve been particularly weak in the Medicare business. Sure, Medicare reimbursement is a low-margin game because of the minimum MLR (Medical Loss Ratio) requirements. But it’s been lucrative for companies with discipline and strong corporate ethics. For a bureaucratic behemoth like Cigna? It’s been a drain, a financial black hole compared to their peers.

That’s why they pivoted to the PBM (Pharmacy Benefit Manager) business. High margins, potential for monopolistic control — it seemed like a no-brainer. The market responded positively at first, and now, Cigna rakes in 70% of its revenues from its PBM operations, becoming the world’s largest PBM in 2023.

What surprises me is that in 14 years of Cordon’s leadership, one of the most risky stocks (in terms of VaR, CVaR, standard deviation, beta, credit risk, etc.) among its peers didn't manage to outperform its peers, even while the stock market was booming. This contradicts the basic principles of Modern Portfolio Theory. Yet, here we are.

One of the reasons for this underperformance is the lack of innovation. When Lisa Gill asked at the J.P. Morgan conference about Cigna's innovations in 2023, Eric Palmer, CEO of Cigna's Evernorth, responded: "the ease of signing contracts". What?

Keep in mind that Cigna keeps referring to Ever north as their "digital health" division. Let me tell ya, there is nothing "digital" about Evernorth or Cigna. Evernorth has essentially become its PBM business, which currently seems to be the most lucrative in healthcare, acting as a middleman between pharmacies and drug manufacturers, and taking a 41% (!) cut of the ‘action’. (Source: Wendell Potter's Substack.)

In April 2020, amid the pandemic’s chaos, Cigna passed on my pitch for an AI solution that could’ve aided thousands of COVID patients. Their reason? They’d just onboarded 200 data scientists to craft their own innovations, brimming with anticipation for their self-proclaimed “great” creation. By the year’s end, they dubbed this expanded team ‘Evernorth’, focusing on “health service solutions”. Fast forward almost four years, and the bitter truth surfaces: Cigna has yet to deliver a single AI product, let alone anything for COVID patients.

2. Cigna Headwinds

📍 When asked at the J.P. Morgan conference mentioned above about the potential threat posed by Mark Cuban’s Cost Plus Drugs and unbundled (transparent) drug pricing to Cigna’s PBM, David Cordani's response was vague, stating something to the effect of, "Not many clients have the sophistication to unbundle." I disagree. I believe, and hope, that for generic drug prices, pharmacies and patients will fare much better with a PBM like Cigna. In a classic example involving Imatinib, a drug used to treat leukemia and other cancers, PBMs have been charging employers around $9,000 a month for this drug, claiming it to be a huge discount from the branded drug's price of $27,000. Meanwhile, Mark Cuban’s Cost Plus Drugs offers Imatinib for $13! This practice of price gauging is illegal. Plain and simple. Congress must act.

📍 PBM legislation was proposed at the committee level a long time ago and will hopefully pass in 2024. My hope is that this legislation will ban the practice of price control and price gouging by PBMs. It’s about time we call out PBMs such as Cigna for what they are: blood-sucking healthcare middlemen that enrich their executives at the expense of consumers and pharmacies.

📍 Cigna’s VillageMD investment has failed miserably. After decades of exploiting primary care physicians, I’m surprised Cigna didn’t realize that primary care was hard. (Source: “How Teeny-Tiny VillageMD Brought Walgreens Its First Net Loss in 122 Years”.)

3. Cigna's Tactics to Artificially ‘Pump Up’ The Stock Price

Let’s be clear: stock manipulation is a crime. To crack a crime, you just need to follow the money. Sadly, the SEC seems to think Cigna is “too big to fail.” Well, I’m picking up the slack and following the money for them...

As I mentioned in my previous research on Cigna, the board, chaired by David Cordani himself (speaking of conflict of interest!), grew weary of this underperformance. They resorted to semi-legal methods to boost Cigna's stock price, throwing a 'Hail Mary'. In November 2023, Cigna announced a merger with Humana, aiming to inflate the stock price.

Now, let’s be clear about the Cigna-Humana merger talks. I believe they were never serious. In my view, it was a pure ploy to pump up Cigna’s stock price — and maybe Humana’s too. Here’s why:

⛔ The merger was not officially announced but was instead reported as under consideration. (For example: Business Insider.)

⛔ Cigna’s lawyers were careful to use the term “merger” instead of “acquisition” to avoid a flood of short selling from merger arbitrageurs.

⛔ For most of us, merger approvals seem like a roll of the dice. But let’s be real, corporate executives aren’t playing the lottery here. They’ve got a front-row seat to the regulatory opera, courtesy of their million-dollar investments in Washington lobbyists. These execs are in constant chit-chat with the big guns at the FTC and the Department of Justice. They’re not just spectators. They’re players. The FTC slammed the door on two high-profile mergers, Aetna-Humana and Cigna-Elevance (formerly Anthem), on the same day back in 2017. And let’s not forget the barrage of healthcare merger blocks we’ve seen this year. Lina Khan? She’s made a name for herself blocking mergers, although breaking monopolies is a different beast altogether. That requires proactive strategies and real courage, especially with the lobbying juggernauts and the ever-spinning ‘revolving door’ of politics. Cigna knew perfectly well that the FTC wasn’t going to buy their flimsy “abandoning Medicare” and “creating synergies” pitch. The proposed Cigna-Humana merger? It was set to birth the biggest PBM monopoly the industry has ever seen. Let’s not kid ourselves: the PBM industry is already rife with questionable ethics. Cigna was well aware that this merger plan was going to be a hard sell to the FTC, to put it mildly.

⛔ The speed with which the merger talks were reportedly called off — within just seven business days, from November 29 to December 10 — suggests that Cigna executives were aware much earlier that the merger would not go through. That was nothing short of a calculated charade, a blatant maneuver to manipulate the stock price. Plain and simple.

Cigna’s execs probably had a few cozy chats with some Wall Street ‘geniuses’ who pitched them a rather seductive theory: Float a merger rumor, and watch your stock soar to the stratosphere. It’s an old Wall Street adage — while monopoly news are a nightmare for consumers, they’re akin to sweet symphonies for the stock market’s ears. Monopolistic might equals market delight, right? However, these so-called geniuses overlooked a critical fact — the market isn’t blind to Cigna’s bureaucratic behemoth, and by the time any ‘synergies’ from such a merger could crystallize, the PBM industry might be a relic of the past.

Much to the Cigna executives’ dismay, contrary to their Wall Street whisperers’ forecasts, their stock took a nosedive.

Desperate times called for grand gestures. So, they played a double card: First, they publicly dropped the merger idea (a peculiar move, given they never officially announced it) in a bid to reverse their stock’s freefall. Second, and more importantly, they declared the largest stock buyback in their history in December 2023.

Let’s unpack stock buybacks for a moment. Stock buybacks are also called share repurchases. In essence, they’re usually a thumbs-up for the stock price. Here’s why: When a company buys back its own shares, it’s signaling to the market that it believes its stock is undervalued. Conversely, equity financing, where shares are sold or issued to raise funds, often suggests the opposite.

Cigna didn’t actually need to buy back shares. The announcement alone was potent enough. And what an announcement it was — a staggering $10 billion buyback, part of a cumulative $11.3 billion when combined with a previous announcement.

David Cordani and Cigna execs are maestros at manipulating Wall Street analysts. They’ve walked the same educational and professional paths. They knew if Plan A (merging two major PBMs into a monopoly) failed, Plan B (a hefty stock buyback) would certainly electrify the analysts, leading to stock upgrades and a price surge. Stock buybacks are Investing 101.

As expected, Cigna’s stock jumped a whopping 17% in a single day falling the buyback announcement, a Herculean leap for an $80 billion corporate giant. For a couple of weeks, this massive boost acted like a shot of adrenaline, propelling the stock to above-median performance. The board, and especially David Cordani, were ecstatic. However, the rush eventually wore off, leaving Cigna’s year-end performance in the dust, much like the previous five years.

Underperformance is one thing, but resorting to questionable methods to pump up the stock price is, at the very least, unethical.

4. Cigna’s Closest Competitors

According to Cigna's latest proxy statement, DEF 14A, filed with the Securities and Exchange Commission (SEC) on March 17, 2023, the following are Cigna's competitors as defined for the purposes of the Strategic Performance Share (SPS) executive incentive compensation program:

🏦 AmerisourceBergen Corporation (COR)

🏦 Elevance Health (ELV), formerly Anthem

🏦 Cardinal Health (CAH)

🏦 Centene Corporation (CNC)

🏦 CVS Health Corporation (CVS)

🏦 Humana (HUM)

🏦 McKesson Corporation (MCK)

🏦 UnitedHealth Group (UNH)

🏦 Walgreens Boots Alliance (WBA)

5. Cigna’s Executive Compensation

Cigna appears to have taken the 1950s ideas of McKinsey consultant Arch Patton, dubbed 'The Godfather of CEO Megapay,' quite literally. Patton's concept was straightforward: incentivize executives by compensating them with stock-linked awards. However, even Patton never advocated for awards of nearly limitless size, as seems to be the case with Cigna. In fact, decades later, when asked in an interview about the impact of his work, Patton's response was simple: 'Guilty.' (Source: The New York Times.)

Furthermore, in the same SEC proxy statement, Cigna acknowledges that, according to their guidelines, a CEO's equity-related holdings should be 8 times their base salary. Yet, they proudly pay David Cordani a staggering 128 (!) times his base salary to “strengthen the alignment of executives' interests with those of our long-term shareholders”:

So, let me get this straight. Paying David Cordani 8 times his base salary, or $12 million, wouldn't align him with Cigna’s long-term shareholders. But paying him 128 times his base salary, which amounts to $192 million, would suddenly create alignment and motivate him? This is absurd. Does anyone actually read these proxy statements? This is complete nonsense.

Not only is the board (again, led by none other than David Cordani) seemingly proud to pay Cordani 128 times his base salary, but they are also enthusiastically urging shareholders to approve this exorbitant pay package:

6. How Did David Cordani Become a Billionaire?

David Cordani is the only CEO billionaire I’m aware of who is not a founder, an inventor, nor in a family business, but rather has amassed his wealth from his company paycheck. This is truly astonishing.

Cordani began his career at Cigna in 1991 as a 'regional leader,' according to his LinkedIn profile. His official compensation was first filed with the SEC in 2005. Therefore, I made some assumptions for his pay from 1991 to 2004. It's worth noting that this period was not as impactful on Cordani’s overall pay as the more recent years, so these assumptions did not significantly alter the analysis.

Specifically, I assumed that for the part of 1991 Cordani worked at Cigna, and for the entirety of 1992, he earned $300,000. Then I linearly interpolated his earnings up to 2005.

Here's a history of David Cordani’s paychecks from Cigna:

Keep in mind that what is reported in the company's proxy filings, while technically accurate, often underestimates total executive compensation. For example, stock-based compensation such as stock options is priced by Cigna using the theoretical Black-Scholes formula. Having written my Ph.D. thesis on options, I can tell you that the theoretical value of an option is irrelevant unless it is expected to be exercised soon. Instead, I only count the options that were exercised and the stock that was sold by Mr. Cordani in that particular year — essentially, the 'money in the bank,' not a theoretical value.

For Mr. Cordani’s 2023 compensation, which hasn't been officially reported yet, I had to make some assumptions. While we know the value of his exercised options in 2023, we don’t have details about his base salary, bonus, and 'Other' compensation. So, I assumed they were the same as the previous year.

Under 'Unvested,' I include the following items that are Mr. Cordani’s assets, which are not yet 'in the bank':

💲 Value of options vesting after 2023: $5,768,303

💲 Value of stock shares vesting in 2024: $10,515,801

💲 Value of stock shares vesting in 2025: $11,883,962

💲 Estimated value of non-vested equity awarded in 2023: $16,004,476

💲 Value of exercisable options: $70,003,133

💲 Average termination payment, as of 12/31/2022: $57,313,050

💲 Pension benefits, as of 12/31/2022: $1,120,488

Here's a fun fact about David Cordani: it took him 23 years working at Cigna to earn his first $100 million, reaching this milestone at the age of 48. Since then, he's been earning $100 million every 1-3 years.

It's unlikely that Mr. Cordani keeps all this money in cash. With a reasonable assumption about interest, it's easy to see how his Cigna paycheck of $663,318,942 could be in the vicinity of $1 billion.

This would make David Cordani the wealthiest health insurance CEO and possibly the richest non-founder CEO. (Source: Stat News.)

It is indeed very convenient to 'recommend' your own compensation package as the chairman of the board. 'I recommend that I’m paid $1 mi... oh wait... $1 billion dollars.'

Of course, I’m being facetious. Cigna’s compensation committee, consisting of independent directors, decides on executive pay. However, one must question the independence of these directors who are paid by the management of the same company for which they are making compensation decisions. And guess what? David Cordani is both CEO and the Chairman of the Board of that company. This situation certainly seems like a major conflict of interest.

How are Cigna shareholders OK with all these?

7. David Cordani’s Tax Tricks

Some of you may be asking, “Well, hold on a second, what about taxes? Surely, once taxes are paid, this billion might really only be half a billion?”

And that's precisely why being super-rich in America comes with incredible perks, including numerous ways to exploit tax loopholes that may not be available to the general public.

In the case of David Cordani, depending on the year, his stock-related compensation accounts for anywhere from 80% to 90% of his total compensation. For instance, from 2018 to 2022, the share of his stock-related compensation was 89%. In other words, for the overwhelming majority of his compensation, Mr. Cordani receives preferential tax treatment.

Namely, Mr. Cordani utilizes the so-called Grantor Retained Annuity Trust (GRAT) to significantly reduce his tax liability. (Thankfully, Cigna is required to file Form 4 with the SEC, where this information is accessible.) These trusts offer significant tax advantages, primarily related to estate and gift taxes. Here's how it works:

💰 The transfer of money to a GRAT is considered a gift for tax purposes. However, the value of the gift is not the full value of the assets but a reduced value. This reduction is due to the Mr. Cordani’s right to receive annuity payments from the trust for a specified term.

💰 The present value of these annuity payments is subtracted from the value of the transferred assets, resulting in a lower gift tax value.

💰 Any growth in the value of the assets in the GRAT that exceeds the IRS Section 7520 interest rate passes to the beneficiaries (i.e., a family trust) at the end of the term tax-free! This is where the significant tax advantage comes into play. If the assets perform well (and they have), the excess growth is transferred without incurring additional estate or gift tax.

It's good to be rich!

8. David Cordani’s Termination Clause

It turns out that even if the board hypothetically decides to fire David Cordani for any of the reasons I’ve mentioned, it won’t be easy. Cordani has ensured his contract includes a lucrative termination clause, which apparently is reneged (interestingly, always to his benefit) every year.

Here’s how much David Cordani would receive if he were to be terminated from his CEO role:

💀 Involuntary termination: $37,676,400

💀 Termination upon a change of control: $77,957,089

💀 Early retirement: $52,203,918

💀 Death or disability: $61,414,791

9. Cigna’s History of Violations

Cigna has a long history of “incidents.” Let me highlight some of the most recent ones:

9.1. Cigna sells patients’ lab results and claims information to WebMD.

In early 2021, Cigna began selling patients' lab results and claims information to WebMD, a notorious "symptom checker" platform. Cigna does seek patient consent for sharing this data, but the transparency and ethics of the process remain questionable. Concerns include unclear information about the storage and usage of this medical data, the potential for WebMD to resell the information to other entities, and the overall impact on patient privacy and trust in medical data handling.

9.2. Cigna’s AI stress tool: shitty and potentially hazardous.

Despite having a seemingly robust team of 200 data scientists within its newly formed Evernorth brand, Cigna opted to hire Ellipsis Health in early 2021 to develop the Cigna StressWaves Test (CSWT). Hosted on Cigna’s website, this AI-based application aims to measure a user's stress levels by analyzing their speech, branding it as a “clinical grade” StressWaves test. (Source: Becker’s Hospital Review.)

However, an independent validation study by three professors from Arizona State University, published in Nature in November 2023, revealed significant flaws in the Cigna tool, labeling it as fundamentally flawed and potentially harmful:

1️⃣ The Cigna stress test has zero reproducibility. When a person takes the test twice in the same session, the results vary dramatically, showing a negative correlation of -0.106. (Referenced in Dr. Visar Berisha's tweet and Gary Marcus's tweet)

2️⃣ There is no association between the CSWT results and the Perceived Stress Scale (PSS), an industry-standard validated instrument for stress measurement.

One of the key criticisms is that the CSWT extends its interpretations beyond state psychological stress (acute, transient stress felt at the time of the test) to trait psychological stress (long-term stress patterns), based on a single one-minute speech sample. This extrapolation has been deemed unlikely to be feasible, especially given the tool's lack of reliability and validity in assessing even state psychological stress.

This incident highlights a broader problem in the healthcare industry, where AI tools are often deployed without adequate validation, especially in large corporations like Cigna where the effectiveness of such devices is critical but often inadequately verified.

9.3. Cigna’s AI algorithm automatically denies claims. Cigna “doctors” concur without even looking.

In a lawsuit against Cigna, the company faced accusations of using its PxDx algorithm to systematically deny insurance claims. Allegedly, Cigna's "doctors" used this tool to automatically reject claims without examining patient files. The algorithm, reportedly, took an average of just 1.2 seconds to review a file, leading to automatic claim denials. In a two-month period in 2022, approximately 300,000 claims were denied by Cigna using this algorithm. (Sources: ProPublica, FierceHealthcare)

The PxDx algorithm, developed over a decade ago by Dr. Alan Muney, a former pediatrician, was a focal point of the lawsuit. (Source: ProPublica) Contrary to previous characterizations, it was revealed during the lawsuit that the PxDx tool was not built on artificial intelligence or an algorithm. (Source: FierceHealthcare)

The use of PxDx led to multiple lawsuits, including a class-action lawsuit in California. This lawsuit claimed that Cigna's use of the PxDx algorithm circumvented the legally mandated individual physician review process, resulting in widespread claim denials. (Sources: HealthLeadersMedia, HealthcareDrive) A similar class-action suit was filed in a Connecticut federal court. (Source: FierceHealthcare)

Cigna won to a settlement of $172.3 million, a minuscule fraction (0.35%) of its most recent Q3 2023 quarterly revenue, to resolve these allegations. (Source: ACDIS)

When the worst penalty is as insignificant as paying four-tenth of a cent on the dollar, it actually encourages these healthcare mega corporations to violate the law. We are facing a massive problem with regulatory capture and corruption in healthcare.

10. Wall Street Analysts Are in Bed with Cigna’s Management

An estimated 5,000 to 10,000 sell-side analysts are believed to operate in the United States. Astonishingly, over 90% of them are deemed absolutely useless, producing "cookie-cutter" reports because that’s what they learned during the CFA (Chartered Financial Analyst) program. Over 90% of these analysts cherry-pick financial models and data that provide the best evidence for their Buy or Hold rating. They almost never produce a Sell rating because such a rating would raise eyebrows among their bosses and could get them fired.

So, they lie. It’s a pathetic way to make a living, but it’s an affluent one.

In fact, according to the latest data from FactSet, of the 10,785 ratings on stocks in the S&P 500, 57% were Buy ratings, 37% were Hold ratings, and only 6% were Sell ratings.

Cigna’s analysts are no different. Currently, there are 23 analysts covering Cigna stock. 14 of them give a Buy rating, 9 recommend a Hold, and not surprisingly, none are giving a Sell recommendation.

This picture is not unique to this time period. It has been approximately the same for many years.

However, the reality is starkly different. Out of 28,114 U.S. publicly traded companies since 1926, 58.6% ended up in wealth destruction (Source), and out of 63,785 global publicly traded companies since 1990, 57.7% ended up in wealth destruction for their shareholders (Source).

Another reason for assigning Buy or Hold ratings is to please the management of the company, such as Messrs. David Cordani and Eric Palmer in the case of Cigna. A Buy or even a Hold rating usually results in a pop in the stock price. If you give a Buy rating, company management might invite you to business meetings to offer you the “insights” they supposedly wouldn’t reveal to anyone else. And that’s another strong point for selling their “research”: “Look, I had a long meeting with the company CEO and boy, do I have a scoop for you.”

11. How Did David Cordani “Misrepresent” His Resume?

Keep reading with a 7-day free trial

Subscribe to AI Health Uncut to keep reading this post and get 7 days of free access to the full post archives.