AI Has Failed Radiologists: Why Do Humans Believe Bad Predictions?

No one will remember that AI has been struggling for over a decade. It will finally get it right, and all of us will forget the past mistakes. It's human nature. Unlike AI, humans tend to forget.

The Oscar ceremony was held last night. Can you name a movie outside of “Barbie” and “Oppenheimer” that was nominated for an Oscar? Most people can’t, despite these being very good movies that have made it onto a very short list of the best movies in the world.

And it’s only been one day. Imagine human memory in a year, 5 years, 10 years. We humans tend to only remember “winners.” We don’t remember second places.

We like winners. We like “visionaries.” We worship them. We elevate them high into the sky. Then we realize that the emperor is completely naked. But by that time, it could be too late.

The problem is, for the life of us, we can’t pick winners. So, we bet on those who behave like winners: those who speak with confidence and look good. That’s it. You don’t need anything else.

We’re so mesmerized by perceived “winners” and self-proclaimed visionaries, we forget to ask very basic questions. But the worst part is, regulators forget to ask very basic questions.

I would like to explore who we, the people, put on a pedestal and whom we call “genius,” “guru,” “visionary,” without checking “under the hood,” and then later become cheated on and lose a lot in the end: money, trust, belief.

So what do portfolio managers, Wall Street analysts, venture capitalists, Bernie Madoff, Elizabeth Holmes, Ali Parsa, Nassim Taleb, Vinod Khosla, and Geoffrey Hinton have in common? Let’s find out.

Portfolio Managers, aka “The Market Beat Us”

Many people believe that portfolio managers (PMs) are geniuses capable of “beating the market.” The truth, however, is often far from this perception. More often than not, the current portfolio under a PM’s management is neither their first nor their second attempt. In fact, a closely guarded secret of the asset management industry, one that retail investors are not supposed to discover, is that the overwhelming majority of portfolios, mutual funds, or hedge funds have been closed and erased from records, never to be featured in the marketing brochures and advertisements of asset management companies again. The reason for this is quite straightforward: those portfolios lost money.

Once portfolios are shut down, uncovering their historical records and identifying the managers responsible becomes an arduous task, even for academic researchers. It’s as if these portfolios never existed, which is truly astonishing.

18,000 portfolio managers and 10,000 Wall Street analysts have been wrong in their investment and portfolio management advice 94% of the time. Not only have they retained their jobs, but they also command some of the highest compensations in the world.

A recent S&P report underscores the absurdity of the situation. Approximately 90% of portfolio managers have made wrong investment choices over the past 15 years across various investment styles and asset categories. (Source: S&P Global.) The investment mandate of active managers is to outperform their benchmark. That’s the Wall Street’s “rationale” behind the hefty hedge fund fees and mutual fund expenses. Yet, 9 out of 10 have failed. Most haven’t even lost their jobs. No apologies were given for their underperformance. When their losses became egregious, resulting in class-action lawsuits like those in 2008, they simply “settled” without admitting guilt or apologizing.

Why is this issue not gaining more attention? The claim of “superior” stock picking and “exceptional” active management underpins the $100 trillion active management industry! (Source: BCG.) This lie, that they can consistently outperform the market, is precisely why hedge funds and the asset management divisions of big investment banks exist.

These “Too Big To Fail” Wall Street institutions won’t admit that 9 times out of 10, you’re better off ignoring their advice and investing in an index. They employ massive lobbying efforts on Capitol Hill and even have their own analyst certification body, the CFA Institute, which has monopolized finance education since 1947. Without the coveted “CFA” designation on your resume, progressing in a Wall Street career becomes incredibly difficult. And guess what’s heavily emphasized in the CFA curriculum? The importance of stock picking and active management – exactly what hedge funds and Wall Street investment banks want propagated.

Thus, reports like the S&P's, or any data that casts doubt on the efficacy of the active management industry, rarely get spotlighted on CNBC, Fox Business Network, or Bloomberg. Boring index investing doesn’t generate viewer ratings. “Star” investors do.

This massive underperformance holds true, and to a much worse extent, for private equity and venture capital managers. But that’s the topic of my next research…

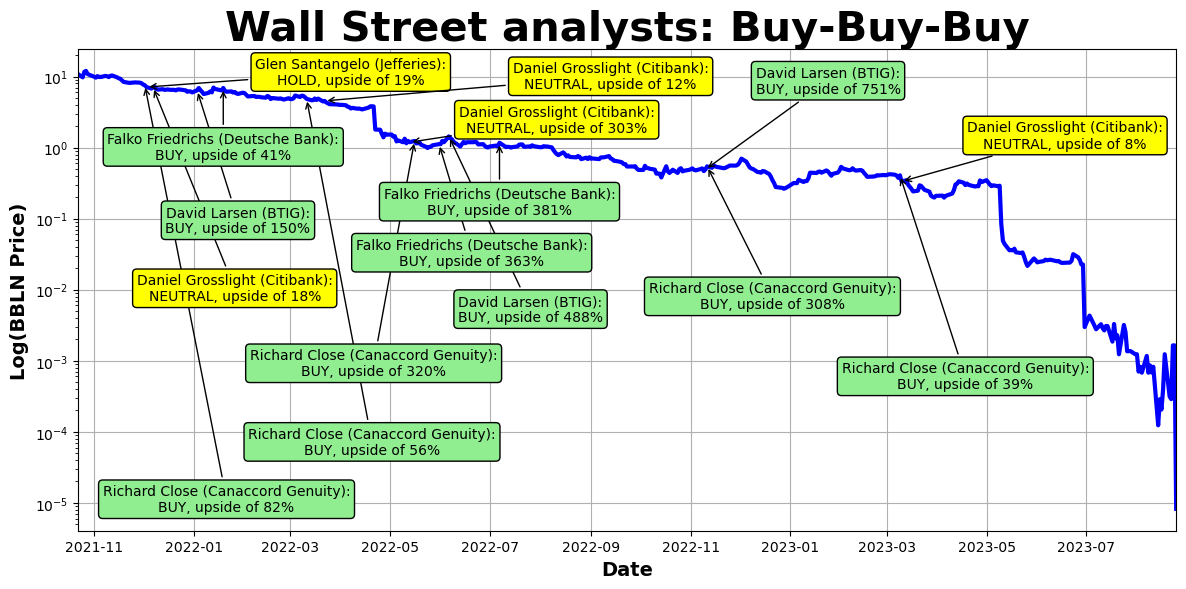

Wall Street Analysts, aka “The Confident Liars”

The so-called sell-side analysts move stock prices every time they issue a report or make a recommendation. Every. Single. Time.

But does their track record justify such influence? Far from it.

An estimated 5,000 to 10,000 sell-side analysts are believed to operate in the United States. Astonishingly, 99% of them are deemed absolutely useless, producing “cookie-cutter” reports because that’s what they learned during the MBA and CFA programs. Over 90% of these analysts cherry-pick financial models and data that provide the best evidence for their Buy or Hold rating. They almost never produce a Sell rating because such a rating would raise eyebrows among their bosses and could get them fired. Why would they risk giving a Sell rating to a company on which their livelihood depends?

So, they lie. It’s a pathetic way to make a living, but it’s an affluent one.

The most notorious among them was Henry Blodget, who worked as the Merrill Lynch Internet analyst during the dot-com era. He famously assigned his stocks a “Buy” rating for the public, but internally he was labeling them as “POS” (piece of shit), advising Merrill Lynch portfolio managers to steer clear of these stocks. (Source: Wikipedia.)

In fact, according to the latest data from FactSet, of the 10,785 ratings on stocks in the S&P 500, 57% were Buy ratings, 37% were Hold ratings, and only 6% were Sell ratings. The Sell ratings are heavily skewed towards large investment banks. An analyst from a smaller research firm would seldom give a Sell rating because that could literally tank the company they work for.

Well, perhaps that’s actually close to the distribution of winners and losers in the stock market? Not even close. On an average year, 40% of companies in the S&P 500 have negative returns, not 6%. In 2022, 48% of S&P 500 companies had negative returns. In 2021, 28% of S&P 500 companies had negative returns, despite 2021 being one of the best years on record, with the S&P 500 returning 29%! This means that 28% of the S&P 500 companies underperformed the average by at least 29% in 2021! But you could have never guessed that by looking at the Wall Street analyst ratings.

However, even this percentage of companies with negative returns is biased downwards due to the so-called “index reconstitution bias” - every year, an index such as the S&P 500 drops a few companies that have been underperforming and replaces them with those who have been performing well. So, a better way to measure underperforming companies is to look at the entire universe of companies, not just the largest 500 U.S. companies. Out of 28,114 U.S. publicly traded companies since 1926, 58.6% ended up in wealth destruction (Source), and out of 63,785 global publicly traded companies since 1990, 57.7% ended up in wealth destruction for their shareholders (Source). The failure rate among private companies and startups is much higher (Source).

Despite all these facts, the narrative these “analysts” have crafted about themselves suggests that each one is exceptional. And we, the consumers, the investors, take their word for it without scrutinizing the data!

Bernie Madoff, aka “The $65 Billion Ponzi Fraudster”

Bernie Madoff was a highly respected figure in the finance industry, having served as the chairman of the NASDAQ stock exchange. His reputation and status provided him with an aura of credibility and trust. This reputation made it easier for him to attract investors and more difficult for people to believe he could be involved in fraud. Madoff’s firm, Bernard L. Madoff Investment Securities LLC, was considered reputable and had a long history of delivering steady, above-average returns, which further cemented investors’ trust in Madoff.

The $65 billion Madoff Ponzi Scheme came to light when Madoff’s sons reached out to the FBI in December 2008. Before this revelation, whistleblower Harry Markopolos had warned the SEC in 1999, 2000, 2001, and 2005. Despite his repeated red flags, the SEC ignored his warnings, due to an unwritten “code of silence”.

The regulatory agencies - the SEC, NASD, FINRA - tasked with conducting audits and raising inquiries, failed to take any action over decades. This inaction was due to Madoff’s perceived aura of excellence and the respect he commanded in the industry.

Elizabeth Holmes, aka “The Queen of Finger Pricks”

Theranos’ founder, Elizabeth Holmes, claimed that their revolutionary technology could perform comprehensive tests using just a few drops of blood from a finger prick instead of the larger samples drawn from a vein required by traditional methods. This technology was supposed to be faster, cheaper, and more accurate than the existing blood-testing methods.

Of course, that was a lie and a fraud. It was discovered that Theranos had conducted a vast majority of its tests using traditional blood-testing equipment rather than its own devices.

Everyone seemed to have been mesmerized by the charismatic and confident Holmes. The SEC, venture capitalists, investors, and the general public all missed the warning signs.

The $700 million Theranos Medical Technology Fraud came to light through a Wall Street Journal investigation on October 15, 2015.

Once again, the SEC was asleep at the wheel.

Ali Parsa, aka “The Madoff of Digital Health”

Ali Parsa, CEO and founder of Babylon Health, lied about the capabilities of the Babylon app. He also lied about the number of actual app users it actually had. In fact, my extensive investigation into Ali Parsa and Babylon Health uncovered 17 lies by Parsa and 16 signs of fraud at Babylon.

Most strikingly, the situation echoes the Madoff scandal, with many of Babylon’s investors, who collectively lost $1.2 billion in equity and $0.3 billion in debt, being unsuspecting retail investors, ordinary people, and retirees who invested through pension funds or sovereign funds.

Ali Parsa was also quite a “prophet of healthcare innovation”. For instance, he proposed a theory of the “rational pyramid of care,” according to which 9 out of 10 patients would exclusively use the app without ever consulting a doctor, thereby eliminating the need for doctors. (Source: VNV Global Capital Markets Day investor conference, September 27, 2022.)

Moreover, Parsa’s operations bear a disturbing resemblance to the Theranos scandal, showcasing a deceptive demonstration of the app’s functionality that was, in reality, non-existent. It serves as another example of how the allure of groundbreaking technology can lead to egregious oversight and deceit.

And once again, the SEC was asleep at the wheel.

Nassim Taleb, aka “The Black Swan Man”

The “doom and gloom” finance guru Nassim Taleb has branded himself as “The Black Swan Man” due to his claimed ability to predict market crashes. Source: “The Black Swan: The Impact of the Highly Improbable.”) However, he omits from his narratives the fact that he managed not just one, but two hedge funds, both of which he drove into the ground. He essentially predicted a crash for the upcoming year, a strategy that statistically would only prove correct once every 13 years. Following significant losses for his investors, Taleb shifted his career towards writing and positioning himself as a crash prediction expert, proven to be a more lucrative endeavor. Within his publications, he frequently discusses the 2001 Dot-Com Crash and the 2008 Global Financial Crisis, emphasizing his correct predictions, yet neglects to acknowledge his numerous failures. Despite this, apart from his investors, many people remember his accurate predictions for 2001 and 2008, overlooking his extensive record of failures.

Vinod Khosla, aka “The Forecaster Without the Horizon”

Vinod Khosla, the co-founder of Sun Microsystems and a venture capitalist, made a prediction in 2012 that AI could replace 80% of what doctors do. He suggested that the healthcare industry could be significantly disrupted by the application of algorithms and artificial intelligence. (Sources: Impact Lab, The Healthcare Blog, Venture Beat.)

In a 2016 paper titled “20 Percent Doctor Included,” Khosla further elaborated on this idea, arguing that a significant portion of healthcare could be automated. He has continued to advocate for the transformative potential of AI in healthcare, predicting in 2023 that within 5 to 6 years, the FDA would approve a primary care app qualified to practice medicine like a primary care physician. (Sources: Khosla Ventures, STAT News.)

None of Khosla’s predictions came true. In fact, the United States is experiencing the largest shortage of human physicians in its history.

Geoffrey Hinton, aka “The Godfather of AI”

By 2016, deep learning had made significant strides, demonstrating remarkable capabilities in image classification, object detection, and other tasks relevant to medical imaging. Deep learning models, particularly Convolutional Neural Networks (CNNs), had become adept at interpreting complex image data, rivaling and sometimes surpassing human accuracy in certain tasks.

The advancements in AI led Geoffrey Hinton, “The Godfather of AI,” to make his notorious prediction in 2016. He claimed that by 2021, the world would no longer need radiologists.

Seven years later, not only the number of radiologists in the U.S. has nearly doubled, but we’re facing major shortages of radiologists worldwide. Furthermore, the currently available AI models in radiology actually degrade the performance of human radiologists, rather than enhancing it. (Sources: Statista, NIH.)

Why Radiologists Are Worse Off Now Than They Were When Hinton Made His Infamous 2016 Prediction?

In a recent research commentary, Dr. Merel Huisman, Dr. Bram van Ginneken, and Dr. Hugh Harvey argue that the AI emperor has very few clothes.

Why is that the case?

1️⃣ Higher costs. By adding narrow AI tools on top of current workflows, no upfront costs are saved since radiologists still must conduct full reads and maintain oversight.

2️⃣ Automation bias. Automation bias refers to the concept of human overreliance on automated decision-making systems. Human-machine interaction, an emerging research area, is increasingly recognized for its potential synergy and errors in diagnostic imaging. For example, Dratsch et al.’s study revealed that radiologists at all experience levels performed worse in terms of speed and accuracy when misled by incorrect AI mammogram results.

3️⃣ Miscalibration. Another recent study showed that AI-assisted readers tend to be biased towards the diagnostic performance of the AI tool, even if the tool is not calibrated to the prevalence of their population. This is not just costly. It creates all sorts of risks for radiologists and for patients.

4️⃣ ‘Complexity overhead’. Complexity overhead is a phenomenon where technical advancements inadvertently add complexity, increasing costs, safety concerns, and ecological impact, according to Borycki et al. This complexity can contra-dict the intended improvement, especially consider-ing the historical trend in radiology where technological advances have escalated workloads due to increased quantity and complexity of imaging studies, according to Kwee and Kwee.

The authors conclude that “we should not fall victim to the shiny object syndrome remaining vigilant about the risks outlined above, conducting structured evaluations, and adhering to established guidelines (e.g., DECIDE-AI).” They advocate “for safe task automation over marginal quality improvements”.

Conclusion: The Peril of Cognitive Biases

Humans are constantly bombarded by advertisements and promotions. They come to believe that someone is a “genius,” a “guru,” a “visionary,” simply because their friends, neighbors, and community hold that belief. This "herd mentality" suffices to cement such opinions. There’s no perceived need to verify facts. This “bandwagon effect” consequently fosters the “halo effect” – a cognitive bias where an observer’s overall impression of a person, company, brand, or product colors their perceptions of that entity’s character and statements.

These biases can be profoundly dangerous. Individuals and entities are elevated, heralded as “geniuses,” “gurus,” “visionaries,” worshiped and trusted by many. Importantly, their actions and predictions often go unscrutinized due to this widespread acclaim. While sometimes the consequences are benign, the failure of fiduciary duty and due diligence by various parties, including regulatory agencies, can lead to heinous crimes and substantial financial losses for investors, both affluent and ordinary.

Do your homework. Keep your biases in check.

👉👉👉👉👉 Hi! My name is Sergei Polevikov. In my newsletter ‘AI Health Uncut’, I combine my knowledge of AI models with my unique skills in analyzing the financial health of digital health companies. Why “Uncut”? Because I never sugarcoat or filter the hard truth. Thank you for your support of my work. You’re part of a vibrant community of healthcare AI enthusiasts! Your engagement matters. 🙏🙏🙏🙏🙏